Who knew a single footnote could create so much noise! I'm heading to American Bankers Association Risk and Compliance Conference (RCC) tomorrow. They asked me to speak on genAI and how it is impacting fair lending. I'll be opening up with what I call "The Infamous Footnote". It's a fairly beefy three sentence paragraph at the bottom of a very recent supervision and regulation letter, SR 26-2 put out by the Board of Governors of the Federal Reserve System.

It's funny, I read this whole document with a critical eye, only to get to the end, puzzled. Nothing in the body of the letter said anything at all about generative AI. With my handy friend Claude, I was then led to the page with The Infamous Footnote (highlighting mine).

Fair lending is the body of law that says credit decisions can't be based on who someone is, only on whether they can repay the loan. It applies to every step of the credit lifecycle. The two main federal statutes are the Equal Credit Opportunity Act (ECOA), which covers all credit, and the Fair Housing Act (FHA), which covers housing-related credit specifically.

To comply with fair lending requirements, you have to design every stage of credit so it doesn't treat protected classes differently and doesn't use "facially neutral" features that act as proxies for protected status. You have to test your actual outcomes for disparities, document why any disparity that exists is justified by business necessity with no less-discriminatory alternative available, and produce specific principal reasons whenever you take adverse action against a consumer. And you have to prove all of that on demand - to examiners, to plaintiffs, to your own board - through inventories, written policies, monitoring records, vendor due diligence, and a paper trail that lets someone reconstruct any single decision from application to outcome.

Let's take a generative example and walk it all the way through. ACME mortgage is releasing a generative pre-qualification chatbot on its website in response to customer requests for more self-service options. The goal of the chat both is to engage conversationally with the human, discern the humans intent, and then provide a set of options for which that human might be eligible. Ultimately, the lender could decide to implement this use case in a lot of different ways - with human in the loop, intersecting LLM with more deterministic solutions, there are many options - for our example, let's say the chatbot is autonomous.

The lender would need to design the chatbot so that is does not use things like name or zip code to steer a homeowner into a more expensive product. You need name to pull credit. Zip code is necessary to determine property location and estimate property taxes. Name and zip code are both necessary to pre-qualify a borrower (with credit). Name and zip code are both known "race proxies" in mortgage, variables that looks race-neutral but carry enough racial signal that using it produces the same effect as using race directly. The lender is allowed to use name to pull credit and ZIP code to identify the property and estimate taxes.

What the lender cannot do is let those variables shape the chatbot's product recommendations, rate quotes, or routing — because that's where they would function as race proxies in a way the law treats as discrimination. If the chatbot outputs nonetheless show different outcomes by protected class, the lender's defense is to demonstrate that the design was justified by business necessity and that no less-discriminatory alternative would have served the same need.

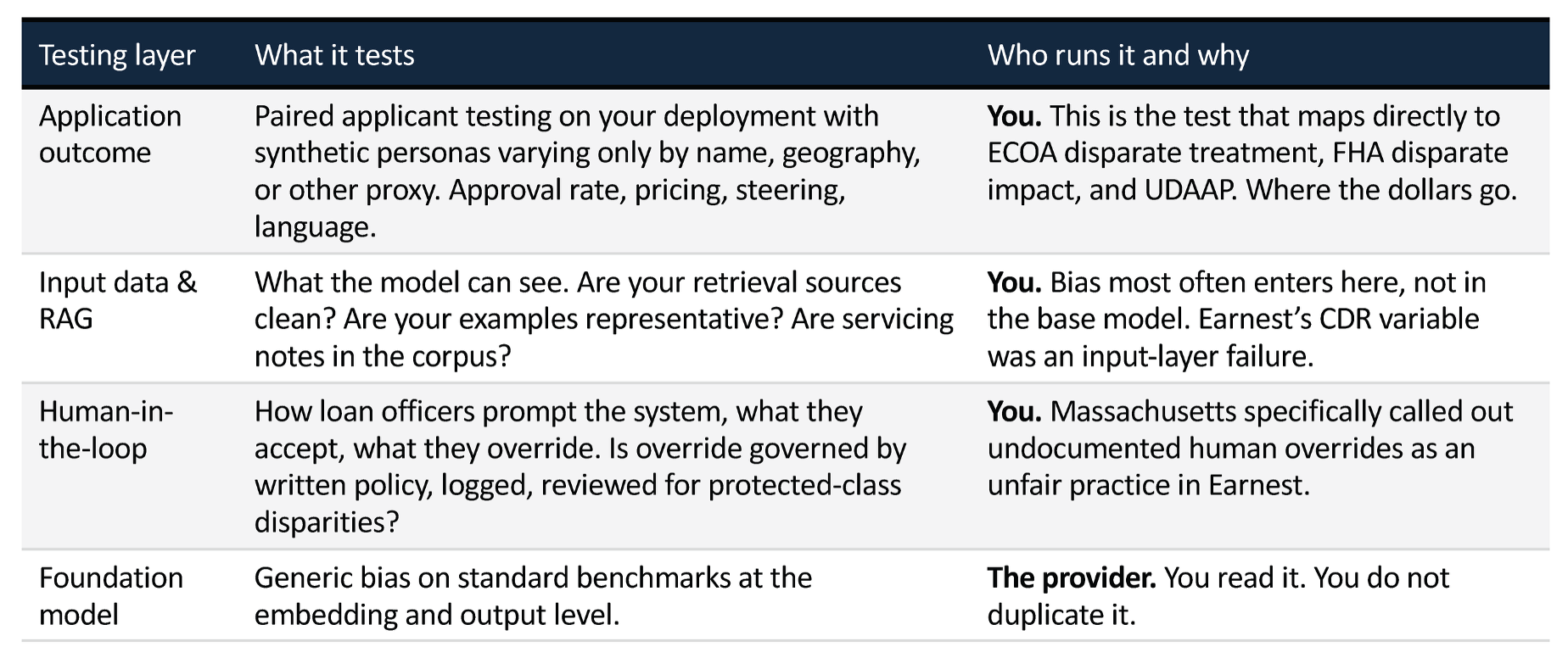

In this case, there are two levels of potential for bias to be introduced: (1) the actual application the lender's technology team built to deliver the chatbot to the human, and (2) the underlying foundational model that is discerning intent, potentially deciding request flow, and producing language.

The introduction of generative models like large language models introduces a significant new variable into the testing equation, especially fair lending testing.

When using a large language model at scale, there are two primary roles. The deployer and the developer. The developer is called a foundation model provider - think Open AI with ChatGPT, Anthropic with Claude. They develop the models and make them available for use. YOU as the lender, servicer, regulator, or other mortgage industry actor are the deployer. You are actually giving the model to some set of users to derive benefit for the organization, the homeowners, whomever the target user base is.

As the deployer, you need to understand what types of bias testing the foundation model provider does - the very common ones are BOLD (Bias in Open-ended Language Generation Dataset) and BBQ (Bias Benchmark for QA). It is good to understand these tests, and understand how (or if) they impact your use cases. That's for you to figure out.

You are solely responsible for fair lending testing on the application, in our example the chatbot. What kind of testing are you obligated to do? This is where the footnote comes in. There is no rulebook for how to test, govern, monitor, or evaluate solutions that incorporate generative solutions. The footnote is really quite unhelpful. First it says generative AI and agentic AI are "out of scope". Then it says your current practices "should guide". And finally it says the principles in the guidance (but not the actual guidance) does apply.

IF, and that's a big if, you decide to implement a pre-qualification chatbot, you should run a standard set of fair lending tests on your chatbot. Follow all the prescribed tests, use all the standard techniques. You should ALSO understand how the generative model is being used in your solution and the extent to which the model capabilities are increasing or decreasing risk. And you should look at what the model providers and any independent benchmarks say about bias testing.

I'll be honest, I don't think an autonomous, generative, pre-qualification chatbot is a good idea right now UNLESS it has a fair amount of determinism in it (so an agentic solution that intersects the intent detection of an LLM with the certainty of a deterministic answering solution).

This is a really challenging topic, with a lot of tentacles. Despite the changes that have happened in the past 12 months, I don't see a responsible way to step back from the traditional practices lenders and servicers have undertaken for fair lending testing. One of the federal requirements has been removed, but the laws are still the laws. The model governance requirements are totally unclear, so we should be cautious in these areas. Be very careful about selecting your use cases. The quadrant chart I provided above gives a good framework, study it carefully and use your best professional (and probably legal) judgment as you make your decisions.

By Tela Mathias, Chief Nerd and Mad Scientist at PhoenixTeam